How to Set Up an SMSF to Buy Crypto

The simple way to hold crypto in your super, and the one mistake that fails an audit.

Table of contents

- Can an SMSF buy crypto?

- Is an SMSF right for your crypto?

- The Checklist for your SMSF to hold crypto

- The 6 steps to set up an SMSF to buy crypto

- Step 1: Choose a provider who knows crypto

- Step 2: Set up your trustee structure

- Step 3: Get a trust deed that allows crypto

- Step 4: Register the fund with the ATO

- Step 5: Open the bank account and set the investment strategy

- Step 6: Open the exchange account and buy your crypto

- Staying compliant after you buy

- Safekeep Case Study on Setting up an SMSF

- What it costs

- How crypto in an SMSF is taxed

- Where to go from here

You like the idea of crypto in your super, working for your retirement, on your terms. But then the doubt creeps in. One wrong move, and the Tax Office could treat your fund as non-complying. That fear is fair. It is also easy to avoid. Setting up an SMSF to buy crypto is a clear process you can follow, step by step. This guide shows you how to do it. But for the full picture of crypto inside super, see our complete guide to crypto in an SMSF.

Can an SMSF buy crypto?

Yes. An SMSF can buy and hold crypto, including Bitcoin. There is no rule against it. To do it the right way you’ve got to meet these conditions:

- Your trust deed allows crypto.

- Your written investment strategy covers it.

- You hold the crypto in the fund’s name, kept apart from your personal crypto.

- The fund buys the crypto itself, with its own money.

- You buy through an exchange that can hold the crypto in the fund’s name, paid from the fund’s bank account. An AUSTRAC-registered Australian exchange is simplest. An overseas exchange works only if it offers an SMSF account.

Get those right, and the rest is simple.

The one mistake that fails an audit

Here is the rule that trips people up. Your fund must buy its own crypto, with its own money.

The ATO is clear on this. Under section 66 of the super law, crypto does not get the related-party exceptions that shares and business property do. So selling or gifting your own coins to your fund breaks the rules. Buy fresh, inside the fund, and you stay safe.

At a glance

| What to expect | Detail |

|---|---|

| Steps to set up | 6 |

| Typical setup time | 2 to 4 weeks |

| Setup cost | about $880 to $4,000 |

| Annual running cost | about $1,300 to $10,000 |

| Yearly audit | required |

Is an SMSF right for your crypto?

An SMSF suits crypto if you are investing for retirement and can carry the yearly cost and the risk. It is a poor fit for a quick trade or a very small parcel, where the running cost can outweigh the gain.

An SMSF has one job: to pay you a retirement benefit. That is the sole purpose test. Every choice the fund makes has to serve it. Crypto fits inside that job, as long as you hold it as a real retirement investment.

Two things to weigh up:

- Crypto moves fast. A fund with most of its money in one volatile asset carries real risk.

- An SMSF costs money to run. You pay for it every year, on top of the audit.

For a small amount of crypto, the admin running can be more than your gains. For a larger, long-term holding, it often pays off. You decide what fits your goals.

The Checklist for your SMSF to hold crypto

These are the deliverables you’ll get after your SMSF is setup and you need them to buy crypto.

- A trust deed that allows crypto.

- An investment strategy that names crypto and sets an allocation.

- A trustee structure, ideally a corporate trustee.

- A bank account in the fund's name.

- An electronic service address (ESA).

- An exchange account in the fund's name.

- A wallet owned by the fund, kept apart from your personal crypto.

- Minuted trustee decisions on record.

The 6 steps to set up an SMSF to buy crypto

- Choose a provider who knows crypto.

- Your provider sets up the trustee.

- Your provider drafts a deed that allows crypto.

- Your provider registers the fund with the ATO.

- Your provider opens the bank account and writes your strategy.

- You open the exchange account and buy your crypto.

Here’s each step in detail.

Step 1: Choose a provider who knows crypto

You don’t set up a crypto SMSF on your own. You choose a provider to do it for you, usually a specialist accountant or SMSF firm. They handle the setup, the registration, and the yearly compliance.

Here is the catch. Most providers can set up a standard SMSF. Far fewer know crypto. Pick one who works with crypto funds every day, writes your deed to allow crypto, and lets you hold the crypto in the fund’s own wallet rather than locking you into their platform. Self custody is critical. More on that later.

To learn more how to choose a provider read: how to choose a crypto SMSF provider.

Step 2: Set up your trustee structure

Your provider sets up the trustee for you. You make one key choice: individual trustees, or a company as trustee. For a fund that will hold crypto, a corporate trustee is the better fit.

Here is why a corporate trustee suits crypto:

- It holds your wallet and exchange accounts in one name on behalf of the fund.

- The name on your assets stays the same when members join or leave.

- It keeps the fund’s crypto clear of your own.

| Individual trustees | Corporate trustee | |

|---|---|---|

| Who holds the assets | Each trustee, jointly | The company |

| Members allowed | Up to 6 | Up to 6 |

| Single-member fund | Needs 2 trustees | Can have 1 director |

| If a member changes | Re-title every asset | No change to asset names |

| Upfront cost | Lower | Higher (company setup) |

| Best for crypto | Workable | Recommended |

Every director must get a director ID before the fund is registered. You apply yourself, online, and it is free. Your provider will walk you through it.

Step 3: Get a trust deed that allows crypto

Your provider drafts the trust deed. The deed is the rule book for your fund. It sets out how the fund runs and cannot override the law.

Your job is to make sure the deed allows crypto. Your investments have to be permitted by your deed to be compliant. So ask your provider for a deed that names crypto, or digital assets, as an allowed investment. A good crypto deed gives the fund clear power to buy and hold coins.

Already have a fund? Ask your provider to review the deed and add that power before you buy a single coin. Sort the deed first, and the rest runs smoothly.

Step 4: Register the fund with the ATO

Your provider registers the fund with the ATO. They apply for an Australian Business Number and a Tax File Number. They also elect for the fund to be regulated, which is what unlocks the fund’s tax breaks.

One thing to know. The fund has 60 days to register, counted from the day it is legally set up. Your provider keeps you inside that window, so register promptly and you are fine.

Step 5: Open the bank account and set the investment strategy

You can now open a bank account in the fund’s name or the trustee on behalf of the fund. Contributions land here, and the fund pays its bills from here. The account name shows the money belongs to the fund. For example:

- Individual trustees: “John and Jane Smith as trustees for Smith Super Fund”.

- Corporate trustee: “Smith Super Fund Pty Ltd as trustee for Smith Super Fund”.

This account matters for crypto, because you pay for your coins from it. Your provider also sets up an electronic service address, or ESA. An ESA is a secure address, not an email, that lets the fund receive contributions and rollovers through the SuperStream system.

Then your provider writes your investment strategy. The law sets out what it must cover: risk and return, how spread out your money is, cash flow, and member insurance.

A crypto plan needs care. The ATO is clear about what passes. The strategy must fit your fund, and it must do more than repeat the law. Planning a big crypto holding? The strategy should show you have weighed the risk of holding a lot in one asset. Your auditor checks that your crypto matches the strategy, so keep it real. Your provider will help you get it right.

Step 6: Open the exchange account and buy your crypto

Now you buy. Your provider helps you open an account on a crypto exchange in the fund’s name. Then you fund it and buy. Three rules keep it compliant:

- Use an exchange that offers an SMSF account, so the crypto is held in the fund’s name. An AUSTRAC-registered Australian exchange is simplest. An overseas exchange can work too, but only if it supports SMSF or entity accounts.

- Open the account in the fund’s name, never your own.

- Pay from the fund’s bank account.

Not every exchange offers an SMSF account, and the paperwork differs. This matters most with overseas exchanges. Many do not support SMSF structures, so the crypto ends up in a member’s personal name, and that is a compliance breach. Use an overseas exchange only if the fund can hold the asset in its own name and still meet the audit rules. Our guide compares the options: opening a crypto exchange account for your SMSF. Once your account is live, you can buy Bitcoin, Ethereum, or other coins, all inside your fund.

One practical tip. Some banks slow or block transfers to crypto exchanges. Check that your fund’s bank is happy with exchange transfers before you start. For more on moving money in and out, see crypto on-ramps and off-ramps.

Staying compliant after you buy

Setting up is the start. Your provider then keeps the fund compliant, year after year. Three things matter most:

- Keep the fund’s crypto separate. The coins live in a wallet or account in the fund’s name, apart from your personal crypto. Mixing the two is a common audit failure.

- Value the crypto at 30 June. You record the market value at year-end, using a reputable exchange price.

- Pass the yearly audit. According to the ATO, every SMSF must be audited each year by an approved, independent auditor. Crypto gets extra checks on ownership and value.

Two areas are worth a closer read. Learn how to store crypto safely in an SMSF wallet, and see exactly what the auditor checks.

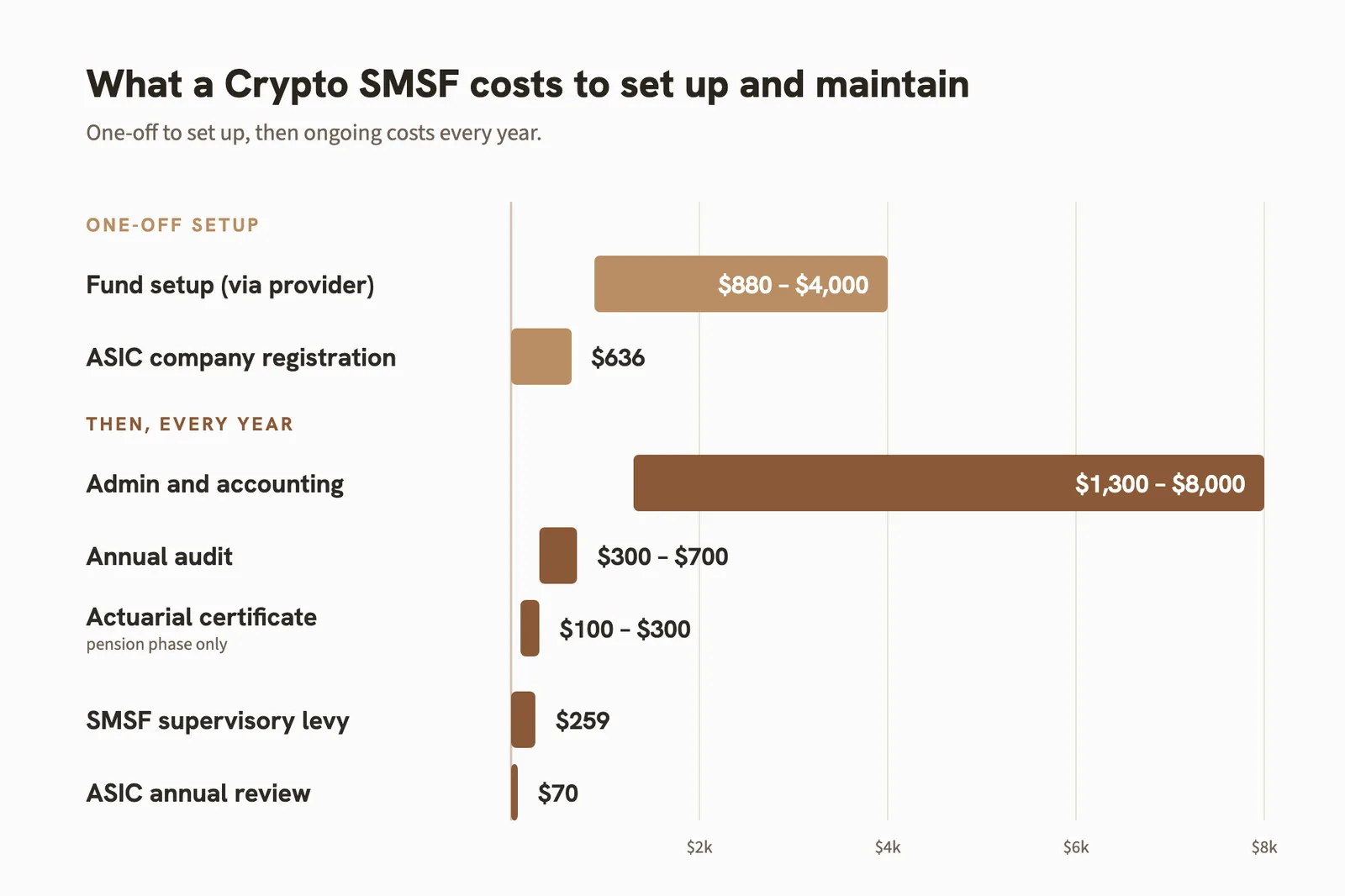

What it costs

Crypto in an SMSF costs money to set up and to run. Setup runs about $880 to $4,000. Running the fund costs about $1,300 to $10,000 a year, depending on how active it is. Here are the 2026 figures. Price is always range based on the complexity of the amount of money, what you’re investing in and how many assets.

| Item | Cost | Notes |

|---|---|---|

| Fund setup (through a provider) | about $880 to $4,000 | Depends on structure and service level |

| Register the trustee company (ASIC) | $636 | One-off, from 1 July 2026 |

| ASIC annual review (special-purpose company) | $70 a year | Lower than the $342 an ordinary company pays |

| SMSF supervisory levy | $259 a year | A new fund pays $518 in its first return |

| Annual audit | about $300 to $700 | Higher for funds with lots of crypto activity |

| Annual admin and accounting | about $1,300 to $8,000 | Crypto and high trade volume push this up |

Cost depends on how much you do yourself. A cheaper, self-service setup leaves more of the record keeping with you. A full-service provider does more of the work and charges more for it. Pick the level of help that suits how hands-on you want to be.

How crypto in an SMSF is taxed

The tax breaks are a big reason Aussies do this. According to the ATO, a complying SMSF pays 15 per cent on its income. Hold an asset for at least 12 months, and a one-third discount cuts the rate on the gain to about 10 per cent. In pension phase, the gain can be tax-free.

A quick example. A $30,000 gain on Bitcoin held over a year is taxed at about $3,000 in accumulation phase. In pension phase, it can be tax-free.

There is more to know. Swapping one coin for another is taxed too, and the ATO matches data straight from the exchanges. For the full detail, read our guide to SMSF crypto tax.

Where to go from here

You now have the whole path to set up an SMSF and buy crypto properly. Build the fund. Confirm the deed and investment strategy allow crypto. Open the exchange account in the fund’s name. Then buy, and hold it where the fund clearly owns it.

The order is what matters. Get it right from the start, and the fund stays compliant and audit-ready. Cut corners, and a single breach can cost far more than the setup ever would.

If one decision shapes all the others, it is who sets it up with you. A crypto-capable SMSF specialist gets the structure right, keeps the fund compliant, and steers you clear of the mistakes that catch DIY trustees.

Setting up an SMSF to buy crypto FAQs

Can I transfer my own crypto into my SMSF?

No. Crypto is not a listed security or business real property, so it falls outside the related-party exceptions in section 66 of the SIS Act. Your fund must buy crypto itself with its own money.

Do I need a corporate trustee to buy crypto in an SMSF?

A corporate trustee is strongly recommended. It holds your wallet and exchange accounts in one name that does not change when members join or leave.

How is crypto taxed inside an SMSF?

A complying SMSF pays 15 per cent on gains. Held for 12 months or more, the one-third discount brings the effective rate to about 10 per cent. Assets backing a retirement pension can be taxed at zero.

Which exchanges support SMSF accounts?

Australian exchanges that offer SMSF accounts include CoinSpot, Swyftx, Independent Reserve, Coinstash, CoinJar and Kraken. Each must be registered with AUSTRAC, and the account must be in the fund's name.

Does an SMSF with crypto still need an audit?

Yes. Every SMSF must be audited each year by an ASIC-approved auditor. Crypto draws extra scrutiny on ownership, existence and value, so keep clean exchange records.

Keep reading

Sources

Primary sources for the facts and figures in this guide, current as at July 2026.

Australian Taxation Office

- Restrictions on SMSF investments (section 66)

- Your obligations as an SMSF trustee (sole purpose test)

- Navigating SMSF crypto assets

- Auditing SMSFs with crypto assets

- Your investment strategy

- Choose your SMSF trustee structure

- Create the SMSF trust deed

- Register your SMSF

- Set up your SMSF bank account

- Get an electronic service address

- Verifying the market value of fund assets

- Your SMSF auditor

- How SMSFs are taxed

- SMSF supervisory levy